Editor’s word: This can be a recurring publish, usually up to date with new data.

When planning a world journey, you are possible utilizing your laptop for on-line purchases in different international locations. And for objects with a restricted provide — like high-demand prepare routes, in style vacationer points of interest and particular guided excursions — it’s crucial to substantiate these reservations earlier than they promote out.

Sadly, you’ll be able to’t at all times depend on your journey bank cards to efficiently full these worldwide transactions. All of it comes right down to the authorized necessities related to bank card safety — which may range drastically, relying on the place you’re going.

In idea, journey rewards bank cards ought to be very best for journey, however more and more refined know-how may have an effect on your upcoming journeys exterior the U.S.

Right here’s what you could find out about bank card safety know-how and what you are able to do to cut back your possibilities of encountering issues alongside the way in which.

What’s 3D Safe?

3D Safe (or 3DS, because it’s generally known as) is a bank card safety know-how that helps confirm the authenticity of on-line transactions. It checks a number of elements to authenticate a purchase order, together with the person’s location, the historical past of purchases on that card and whether or not the private knowledge offered through the transaction matches the financial institution’s data.

If the know-how identifies any abnormalities throughout this verification course of, it could use extra safety checks through textual content message, e-mail or cellphone name earlier than finishing the acquisition.

The purpose of 3DS is to offer higher authentication of transactions to assist everybody concerned: prospects, banks and on-line retailers. Customers profit from an improved expertise with an easier transaction. Banks profit from decreased fraud and chargebacks. And retailers profit by having a neater course of for shoppers in order that they really full the transaction and spend cash with the service provider.

Nonetheless, there’s extra to 3DS than these fundamentals.

Join our day by day e-newsletter

How 3DS took place — and improved

Bank card requirements as we all know them date again to 1995 when three firms — Europay, Mastercard and Visa — got here collectively and created the chip-based EMV know-how added to credit score, debit and pay as you go playing cards. Since then, different banks like JCB, China UnionPay and Uncover have additionally adopted EMV.

EMV continued to evolve over time, ushering in new credit score know-how like contactless card funds.

In 1999, 3D Safe — a extra trendy model of EMV — emerged. Nonetheless, its first iteration confronted some criticism. The principle situation? Browsers redirecting to verification portals appeared fraudulent, and lots of shoppers deserted their transactions. However when an up to date model was unveiled in 2016, it shortly grew to become the brand new business normal for decreasing fraud.

By offering extra contextual data (akin to a card’s transaction historical past and mailing handle) throughout checkout, fewer shoppers questioned the legitimacy of the verification course of. That’s as a result of the revised course of — which restricted the variety of transactions requiring authentication and supported authentication through biometrics or a financial institution’s cell app — lacked the noticeable interruptions or burdens of the previous model.

“Whereas they’re being authenticated and getting the advantages of upper safety, they’re not disrupted of their expertise by way of the movement of the transaction,” stated Ranjita Iyer, Mastercard’s senior vp of cyber and intelligence for North America. “It’s utterly frictionless. Many instances, they don’t even actually see the authentication.”

The place US bank card issuers stand in adopting 3DS

As soon as the revised 3DS know-how’s advantages grew to become obvious, the U.S. started requiring bank card processing networks and issuing banks to make use of it. Nonetheless, the place the fee processors and issuing banks stand on implementation is unequal. Retailers within the journey sector have adopted 3DS at the next fee than retailers in different classes, in accordance with Iyer.

For instance, Mastercard helps the most recent protocols at scale for each issuer of Mastercard merchandise within the U.S. and helps implementation for each service provider desirous to take part in authentication throughout transactions, in accordance with Iyer.

At Wells Fargo, the most recent iteration of 3DS has been utilized throughout all of its shopper and small-business bank cards, in accordance with an organization spokesperson. When authentication is required for a transaction, Wells Fargo cardholders can select to obtain a code through SMS or a notification within the Wells Fargo app.

Likewise, Uncover has totally applied the second-generation model of 3DS through a proprietary product known as ProtectBuy, in accordance with an organization spokesperson.

Nonetheless, the identical can’t be stated for American Categorical playing cards issued by different banks. “We’re persevering with to work with our financial institution issuing companions and third-party suppliers as they uplift their playing cards to be SafeKey 2.0 suitable,” Kieley stated.

What to anticipate in different international locations

Regardless of most U.S. issuers making strides in implementing 3DS know-how — word that it isn’t required for U.S. retailers — the identical can’t be constantly stated for different international locations.

Throughout the European Union, 3DS is necessary for all on-line transactions. Moreover, international locations together with the UK, Bangladesh, India, Malaysia, Nigeria, Singapore and South Africa require 3DS for on-line transactions.

Nonetheless, others like Australia have blocked prior makes an attempt to make 3DS necessary. The chief justification was further prices that might be handed on to shoppers.

Curious to see what 3DS is like in different international locations and if any points come up when utilizing sure bank cards for on-line purchases, we determined to check transactions for 2 in style vacationer locations: Greece and Japan.

Vacationer websites in Greece

First, we tried to buy tourism tickets for the Agora in Athens from the Hellenic Group of Cultural Sources Growth.

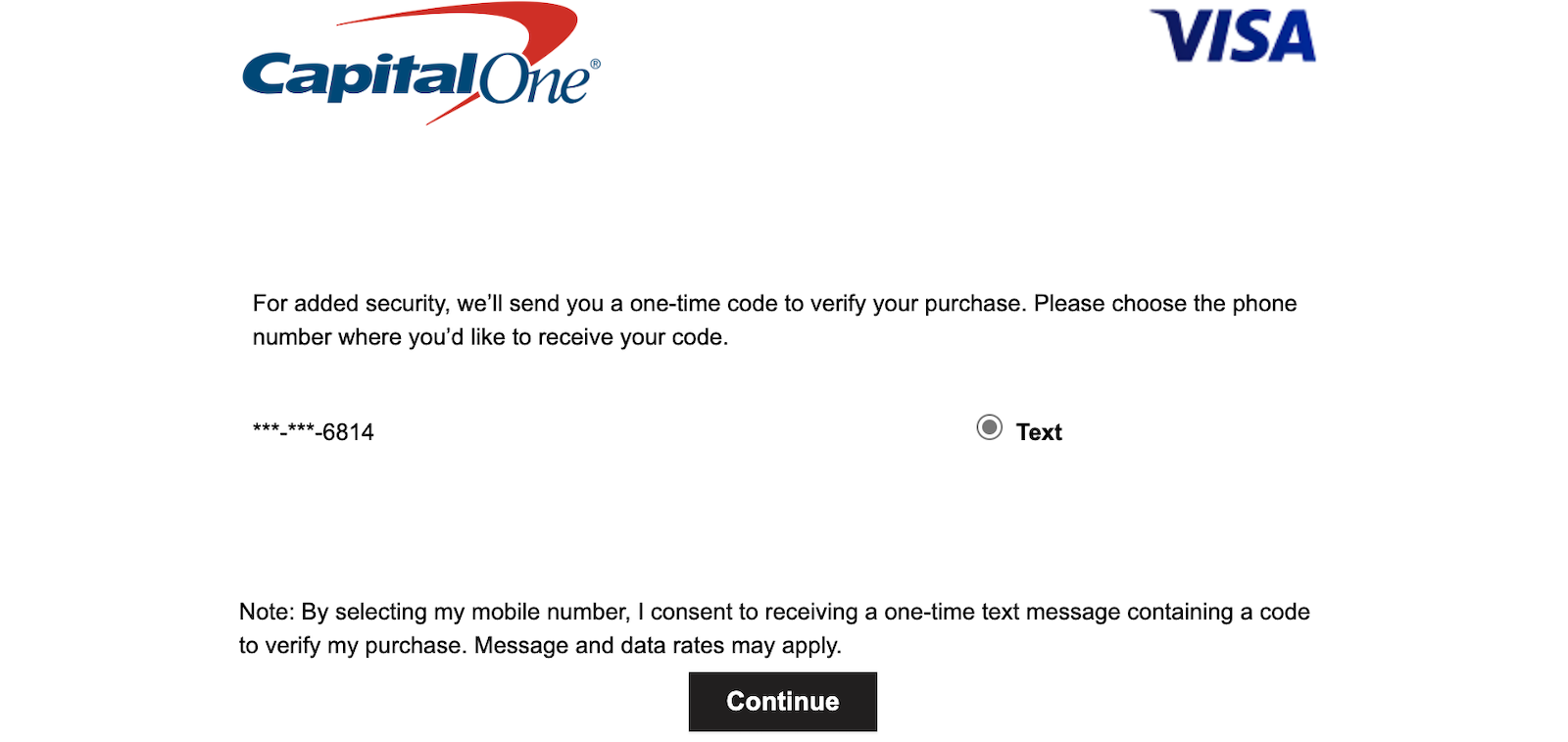

Our first buy used Capital One Enterprise X Rewards Credit score Card. The ticketing web site required verification with a one-time code despatched through textual content message.

Purchases with the Chase Sapphire Reserve (a Visa card), the World of Hyatt Credit score Card (a Visa card) and the Barclaycard Arrival Plus® World Elite Mastercard® handed and had been frictionless.

I acquired an error message when making an attempt to purchase tickets with my Alaska Airways Visa® bank card.

The knowledge for the Barclaycard Arrival Plus has been collected independently by The Factors Man. The cardboard particulars on this web page haven’t been reviewed or offered by the cardboard issuer.

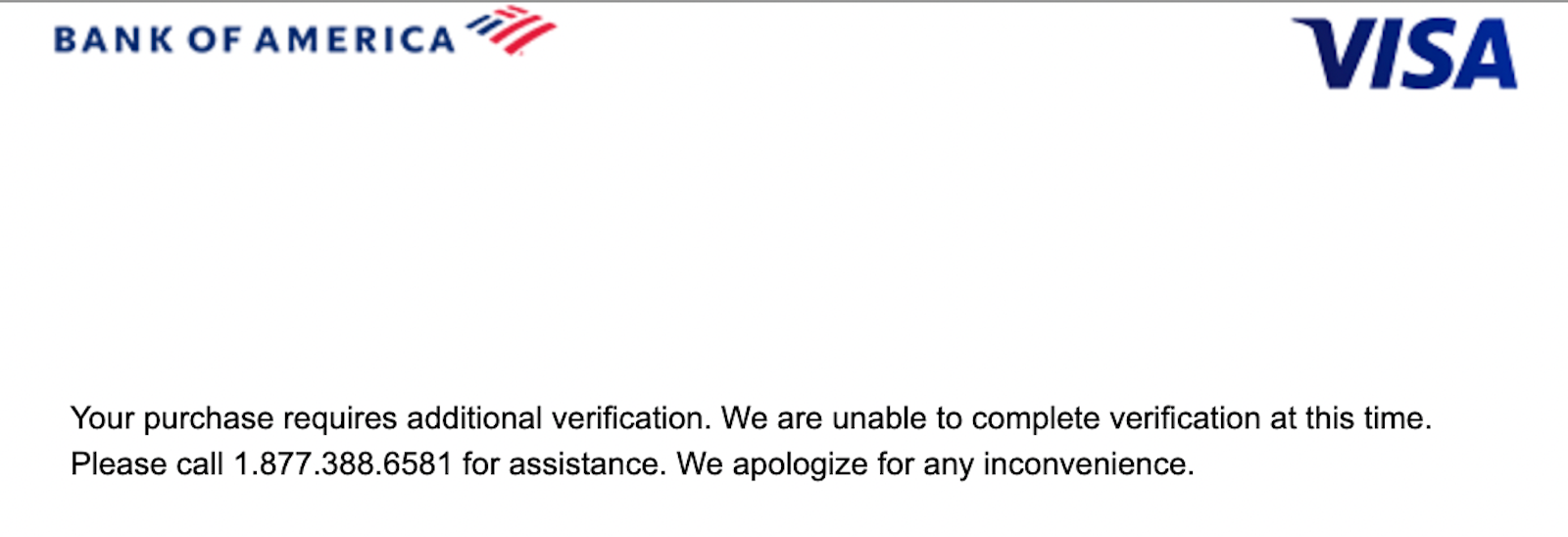

Financial institution of America flagged the acquisition as doubtlessly fraudulent. I needed to name to finish a multi-step verification course of earlier than the financial institution would authorize the transaction. Nonetheless, the web site timed out throughout this course of, and I needed to begin my ticket buy once more from the start.

We couldn’t check any American Categorical playing cards, as the web site doesn’t settle for them for purchases.

Prepare tickets in Japan

We tried to buy bullet prepare (Shinkansen) tickets from Japan Railways Good Ex for Japan. Earlier than buying these tickets, you need to create a person profile and register a default fee technique. The web site particularly states that the cardboard should meet 3DS necessities earlier than you’ll be able to add it to your profile.

I tried so as to add three totally different Visa playing cards — the World of Hyatt card, the Chase Sapphire Reserve and the Alaska Airways Visa bank card — to my person profile throughout registration. All three failed. An error message acknowledged that the issuing financial institution had not arrange the required safety protocols for 3DS authentication.

Subsequent, I attempted The Platinum Card® from American Categorical. After including it to my profile, the web site routed me to American Categorical’ middleman web page (SafeKey). The request processed for a couple of seconds earlier than I acquired a “success” message and was routed again to the Good Ex web site.

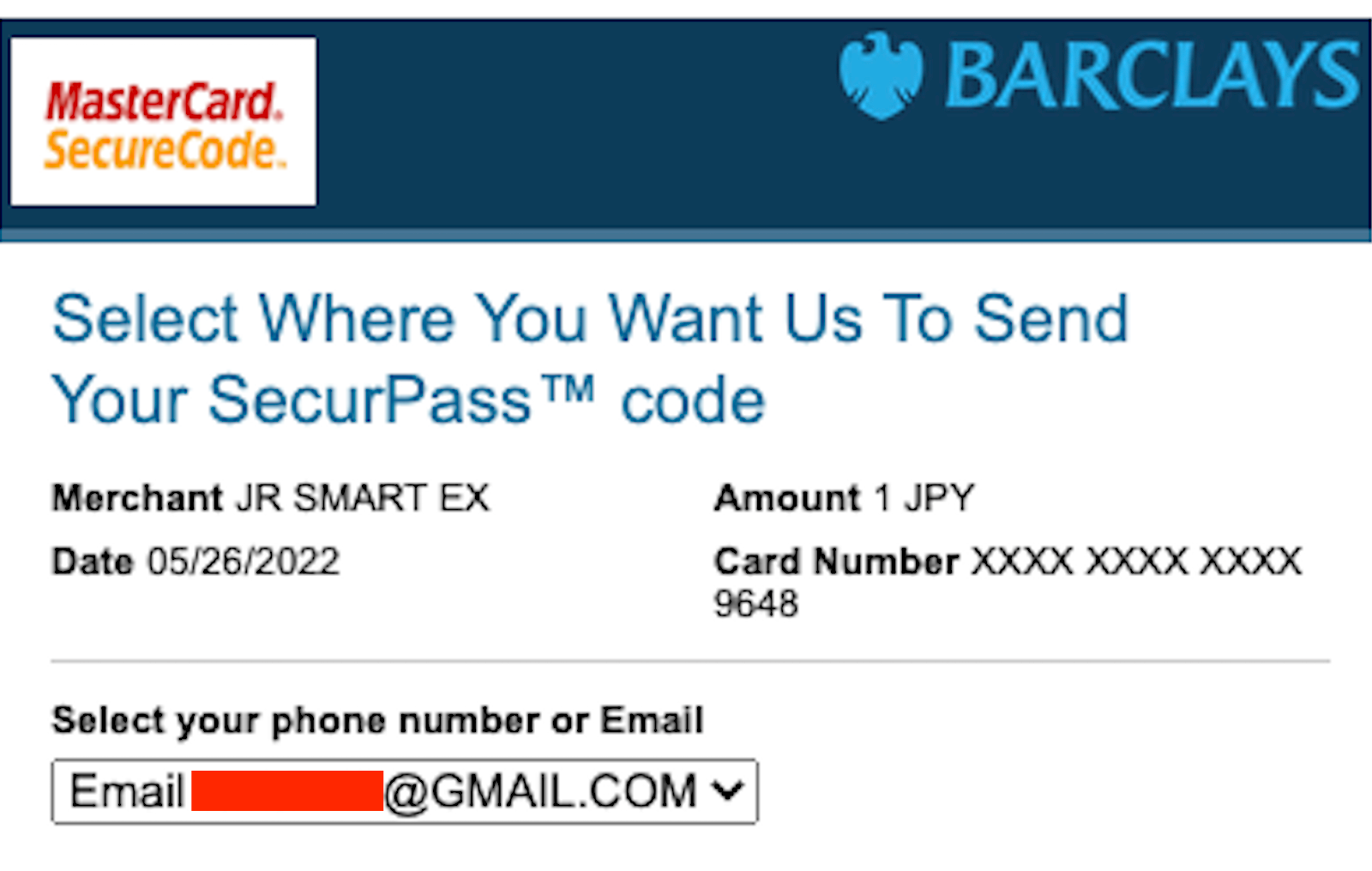

Including my Arrival Plus card to my profile generated the same response because the Amex Platinum. I used to be routed to the SecurPass web site, the place I acquired a one-time code through e-mail.

This can be a very combined bag of outcomes. A few of the hottest playing cards for journey purchases required extra verification. Others merely could not be used with choose worldwide retailers.

What you are able to do to cut back or keep away from points

We requested the bank card issuers what recommendation they’ve for individuals experiencing authentication issues.

Uncover’s spokesperson instructed usually checking and updating your contact data on file together with your financial institution since that’s how the financial institution will contact you if authentication is required. Having incorrect data on file can also improve your odds of a transaction being flagged as fraudulent. It can look suspicious if the handle and cellphone quantity you present through the on-line buy don’t match what your financial institution has on file.

Do you have to run into points whereas making a web based buy, think about contacting the service provider instantly, in accordance with a spokesperson for Wells Fargo. It is because the service provider’s acceptance insurance policies (not the financial institution’s or bank card issuer’s) are possible behind the difficulty you’re experiencing. If this doesn’t work or proves too time-consuming, the spokesperson recommends discovering one other method to pay.

Backside line

Understanding the safety features constructed into your bank card and the way these work together with legal guidelines in different international locations will help you mitigate potential points when utilizing your bank card overseas. It can also scale back the probabilities you encounter an issue utilizing your bank card for on-line purchases associated to an upcoming worldwide journey.

All banks and bank card processing networks within the U.S. require 3D Safe, so your bank cards ought to be accepted and never require further authentication. Nonetheless, that doesn’t imply the service provider (the place you make a fee) will at all times interpret the foundations accurately. Making certain your contact data is up to date together with your bank card firm will aid you cross further safety authentication if prompted.