Editor’s observe: This submit has been up to date with new data.

In the event you’re serious about making use of for a brand new bank card, there are a lot of elements to contemplate. For instance, you could resolve whether or not you need to earn cash-back rewards, resort factors, airline miles or transferable factors in alternate for the purchases you make. And also you’ll must resolve whether or not it’s value paying an annual payment to unlock premium perks, resembling airport lounge entry or assertion credit.

But it surely’s additionally important to grasp a number of issues about credit score earlier than you apply for a brand new card. In spite of everything, it’s doable to make important errors with journey rewards bank cards that may have an effect on your credit score for years to return.

So, at present I’ll talk about seven issues you need to perceive earlier than making use of to your first (or subsequent) rewards bank card.

Associated: TPG’s newbie’s information to bank cards: All the pieces it is advisable know

Know your credit score rating

Once you apply for a brand new bank card, your credit score rating performs a big position in whether or not or not the financial institution approves you.

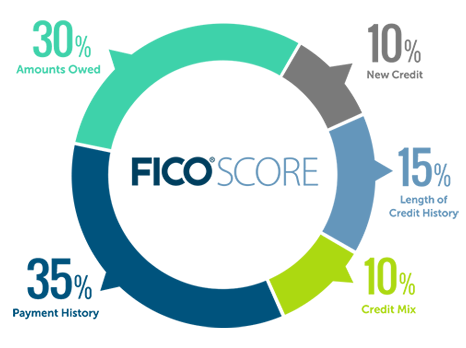

Two of probably the most generally used rating varieties are FICO and VantageScore. Though the precise formulation used to calculate these rating varieties aren’t publicly obtainable, FICO states its scores are based mostly 35% on cost historical past, 30% on quantities owed, 15% on the size of credit score historical past, 10% on new credit score and 10% in your mixture of credit score.

Associated: FICO vs. VantageScore: What’s the distinction and why does it matter?

You possibly can – and will – test your credit score rating often. Fortunately, there are a lot of methods to test your credit score rating free of charge.

Join our each day e-newsletter

For instance, many bank cards supply a free FICO rating to cardholders. However you may as well request your credit score report free of charge from every of the three main credit score reporting companies each 12 months. By inspecting your credit score report, you possibly can test that the data used to calculate your credit score rating is correct.

Banks and different lenders use your credit score rating to find out your creditworthiness. However having a very good credit score rating not at all ensures a call in your favor. Even with a superb credit score rating, you might nonetheless get declined for a particular bank card. In spite of everything, bank card corporations additionally contemplate different elements when deciding whether or not to approve your utility.

Nevertheless, figuring out your credit score rating ought to inform your bank card technique. For instance, in case you have a low credit score rating, you might want to start out with a pupil or a secured bank card to construct up your credit score. And as soon as you already know your rating, you possibly can work to enhance your credit score rating.

Associated: How does making use of for a brand new bank card have an effect on my credit score rating?

Keep away from carrying a stability

That’s why TPG’s first commandment of bank cards is to pay your assertion stability in full month-to-month. Doing so will hold your credit score rating in test and prevent cash.

In the event you’re in a state of affairs the place you might be presently carrying a stability on a number of bank cards, your precedence shouldn’t be to earn rewards however to lower your bank card debt. For instance, a stability switch bank card might show you how to keep away from curiosity costs whilst you work to repay your debt.

And utilizing a 0% introductory annual proportion charge (APR) bank card might show you how to finance a big buy when you don’t have the money to cowl it. However usually talking, when you resolve to open a brand new bank card, you need to prioritize paying off your current balances earlier than you begin accruing curiosity on one other card.

Associated: Bank card myths from my childhood I needed to unlearn as an grownup

Take note of your credit score utilization

As famous above, the quantity you presently owe accounts for 30% of your FICO rating. Particularly, the quantity you owe impacts your credit score utilization ratio, which is the connection between your balances and whole obtainable credit score throughout all of your revolving accounts (together with bank cards).

Typically, it’s a good suggestion to maintain your credit score utilization ratio under 30%. So, when you solely have one bank card with a credit score restrict of $10,000, you shouldn’t let your stability rise above $3,000. In case your credit score utilization creeps above 30%, you possibly can decrease it by making a cost in your card. Even when you pay your bank card balances in full every month, you’ll need to guarantee your credit score utilization is ideally under 30% whenever you apply for a brand new bank card.

In fact, whenever you open a brand new bank card or request a credit score restrict enhance, your credit score utilization will drop since you’ll even have extra credit score obtainable. Likewise, when you shut a bank card or get your credit score restrict decreased, your credit score utilization will enhance since you’ll now have much less credit score obtainable.

Associated: How you can maximize your possibilities of being authorised for a bank card

Get and hold a no-annual-fee card

One of many first playing cards you need to apply for in your credit score journey is a no-annual-fee bank card, such because the Capital One VentureOne Rewards Credit score Card. You could possibly get a no-annual-fee card with minimal advantages even when your credit score rating is comparatively low, as some no-annual-fee playing cards are particularly designed for cardholders with poor to common credit score. Nevertheless, utilizing this card responsibly might help you construct credit score and enhance your credit score rating over time.

Plus, you possibly can hold a no-annual-fee card account open for the foreseeable future with out incurring any annual charges. Getting and holding a no-annual-fee bank card might help your credit score rating by growing your credit score historical past size.

Nevertheless, to maintain your account energetic, you’ll need to use your card for at the least just a few purchases annually. For instance, you might cost a biannual subscription to the cardboard and arrange autopay in your account. By organising autopay, you received’t by chance overlook to pay your bank card invoice.

Associated: Why you need to get (and hold) a no-annual-fee bank card

Know every issuer’s guidelines

For instance, Chase’s 5/24 rule implies that Chase won’t approve you for many of its playing cards when you’ve opened 5 or extra private playing cards throughout all banks prior to now 24 months. Because of Chase’s 5/24 rule, I typically advocate including playing cards within the Chase trifecta to your pockets earlier than making use of for different playing cards. Even when you aren’t able to pay an annual payment, the Chase Freedom Limitless and Chase Freedom Flex are wonderful no-annual-fee playing cards to get whilst you’re below Chase’s 5/24 rule.

Different issuers even have particular restrictions. For instance, American Categorical considers not solely whether or not you’ve held a selected card earlier than however even your total conduct opening and shutting American Categorical playing cards when figuring out your eligibility for its welcome bonuses.

Associated: Can you may have multiple bank card from the identical ‘household’?

Don’t overextend your self

In the event you aren’t positive you possibly can meet the spending necessities with out carrying a stability or incurring further bills, don’t apply. In spite of everything, since most issuers prohibit bonus eligibility to as soon as each few years or as soon as in a lifetime, you sometimes don’t need to apply for a card however not earn the bonus. Or worse, you definitely don’t need to spend greater than deliberate simply since you are chasing bank card rewards.

Associated: The last word information to monitoring your progress towards a bank card sign-up bonus

Think about enterprise playing cards

Probably the most frequent misconceptions about rewards bank cards is that it’s important to personal a proper brick-and-mortar enterprise to get a small-business card. However that is totally unfaithful.

Enterprise playing cards are for every type of small companies, together with new corporations and entrepreneurs who might must separate enterprise bills from private bills. Even people with a facet hustle could also be eligible for choose small-business playing cards. In brief, you would possibly qualify for a enterprise bank card with out realizing it.

In case you are eligible for a small-business card, I like to recommend contemplating how a number of enterprise playing cards might match into your bank card portfolio. Particularly, contemplate whether or not you possibly can make the most of any of one of the best enterprise and private bank card combos. In spite of everything, some small-business playing cards supply wonderful sign-up bonuses and distinctive business-focused spending classes.

Associated: What identify ought to I placed on my enterprise bank card utility?

Backside line

In spite of everything, your credit score rating is the main determinant of your creditworthiness when making use of for a brand new card. And having a very good credit score rating can prevent cash.

Further reporting by Ryan Wilcox and Stella Shon.