Editor’s word: This can be a recurring publish, recurrently up to date with new data.

The concept of incomes free flights and lodge stays simply by signing up for the best bank cards appears too good to be true, and there are many myths about the way it all works. When introducing somebody to the world of reward journey, you will have to dispel a few of these misconceptions.

One of the frequent issues individuals consider after they apply for brand new bank cards is that these actions will negatively and completely affect their credit score scores. Whereas it’s true that recklessly opening new traces of credit score and abusing them (i.e., racking up massive balances, carrying curiosity and lacking funds) can damage your credit score rating, there isn’t a long-term affect in your rating from merely opening new accounts.

Since bank card sign-up bonuses are the inspiration of journey rewards, at the moment we’ll have a look at how your credit score rating is affected whenever you open a brand new bank card.

How does making use of for a bank card affect your credit score rating?

Even should you’ve researched and determined which card to begin with, you shouldn’t apply for it till you perceive how your credit score rating is calculated.

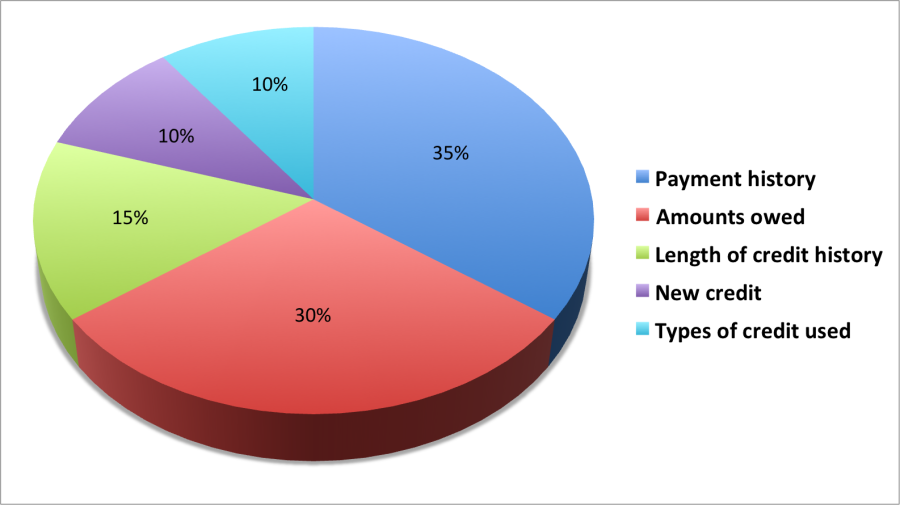

Right here’s a breakdown of the elements concerned:

- Fee historical past (35%): It’s no shock that the class that carries essentially the most weight is your on-time fee historical past.

- Quantities owed (30%): Additionally known as the utilization fee, that is the overall stability on all of your bank cards divided by your complete credit score restrict.

- Size of credit score historical past (15%): Often known as the typical age of accounts, your credit score historical past will end in a better rating the longer it’s.

- Credit score combine (10%): This refers back to the numerous traces of credit score you will have, together with bank cards, scholar loans, a automobile mortgage and a mortgage.

- New credit score (10%): New inquiries in your credit score report account for 10% of your rating.

Associated: How credit score scores work

How can making use of for a bank card damage your credit score rating?

Arduous inquiries vs. mushy inquiries

Your credit score will seemingly be checked dozens of instances all through your life, whether or not you’re making use of for a bank card or beginning a brand new job. There are two various kinds of inquiries, and it’s essential to grasp the distinction.

Arduous inquiries are instances when your credit score is checked in reference to an utility for a brand new line of credit score, akin to a bank card or mortgage. These inquiries get reported to the credit score bureaus and are those that seem in your credit score report — and finally have an effect on your rating.

Join our day by day publication

A mushy inquiry can be should you checked your personal credit score report (to determine should you had been below 5/24 with Chase, for instance) or let your employer examine your credit score as a part of the hiring course of. Tender inquiries don’t get reported to the credit score bureaus and gained’t affect your rating in any approach.

Associated: Does Chase’s 5/24 rule depend inquiries?

How do arduous inquiries have an effect on your credit score rating?

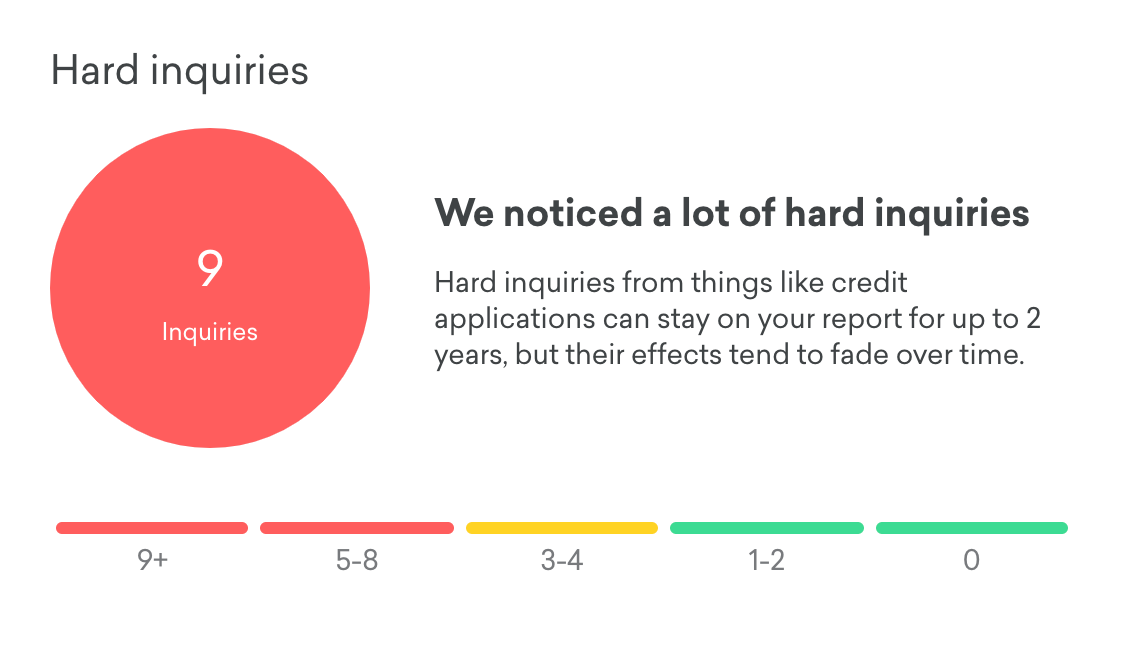

Virtually each time you apply for a bank card, you’ll obtain a tough inquiry in your credit score report. There are some exceptions, akin to the truth that American Specific typically gained’t inquire about current prospects till the brand new utility is authorized. Whereas the precise affect could fluctuate from case to case, usually talking, you’ll be able to count on your rating to drop by about 5 factors every time you apply for a brand new bank card.

This may appear scary should you’ve been working to enhance your credit score rating for a very long time, but it surely’s essential to do not forget that the precise quantity is never what banks have a look at when evaluating your utility. They’ll put you into a spread, say, 700-750 — so in case your rating drops from 740 to 735, it’s unlikely to have any actual impact on future approval odds.

Having too many latest arduous inquiries can drag down your rating. Credit score Karma says that your rating begins to be impacted with three to 4 latest inquiries, however particularly when you get above 5. The inquiry will keep in your credit score report for as much as two years, however the affect fades over time. For those who see a leap in your credit score rating one month that’s not linked to any apparent occasion, akin to paying off a stability, it might be the impact of your inquiries fading in relevance.

Associated: What’s the distinction between a tough and mushy pull in your credit score report?

How can making use of for a bank card assist your credit score rating?

Whereas the arduous inquiry may decrease your credit score rating within the quick time period, opening a brand new credit score line may help you improve your credit score rating in the long term. It offers you with one other alternative to pay your payments in full and on time, which is able to assist your fee historical past because it’s calculated into your credit score rating. It additionally will increase your accessible credit score, which means you’ll be able to extra simply preserve your credit score utilization fee low.

Plus, should you depart the credit score line open, you’ll be able to improve the size of your credit score historical past over time. So long as you employ the brand new bank card responsibly and comply with our 10 commandments of bank card rewards, the brand new card can finally assist your credit score rating.

Associated: Find out how to enhance your credit score rating

Backside line

A vital step in changing into snug making use of for bank cards is studying in regards to the elements that have an effect on your credit score rating and figuring out that the affect in your rating from an utility is minimal. A five-point drop is a small worth to pay if it helps you unlock a sign-up bonus value $1,000 or extra in free journey.

Keep in mind that the drop is barely momentary. Not solely will the impact of the inquiry fade over the course of two years, however in the long run, you may also enhance your rating by persevering with your historical past of on-time funds and rising the typical age of your credit score accounts.

Further reporting by Emily Thompson and Benét J. Wilson.