Your credit score rating performs an enormous function in your general monetary life. We at TPG emphasize sustaining a excessive rating, partly in an effort to be authorized for the perfect bank cards. Usually talking, a credit score rating of 750+ will grant you approval for nearly any bank card available on the market. Nonetheless, you do not have to have glorious credit score to be authorized for a great rewards bank card.

Two frequent playing cards for learners are the Chase Freedom Flex and Chase Freedom Limitless. Each are no-annual-fee bank cards that earn money again — however that money again will be transformed to Final Rewards factors if you even have a Chase Sapphire Most popular Card, Chase Sapphire Reserve or Ink Enterprise Most popular Credit score Card. to benefit from the Chase Trifecta. This basically helps maximize card spending throughout classes for max redemption worth.

Associated: What is an effective credit score rating?

What credit score rating do it is advisable to get the Chase Freedom Flex and Freedom Limitless playing cards?

Though these two playing cards cost no annual charge and are thought of entry-level playing cards, you will nonetheless need to have good credit score to use. Nonetheless, this does not imply it is advisable to have a rating of over 750 to use. Actually, there have been anecdotal reviews of scores within the low- to mid-600s being accepted for each playing cards.

Your credit score rating is unquestionably essential, and you must attempt to enhance it every time potential by practising accountable credit score habits. However you should not let a rating within the mid-to-high 600s cease you from making use of for a card you actually need, particularly when you’ve got confirmed your self to be a reliable buyer in different methods.

Associated: Journey rewards methods for folks with low credit score scores

Easy methods to examine your credit score rating

You need to by no means pay to examine on your credit score rating as there are many choices to examine it reliably without spending a dime.

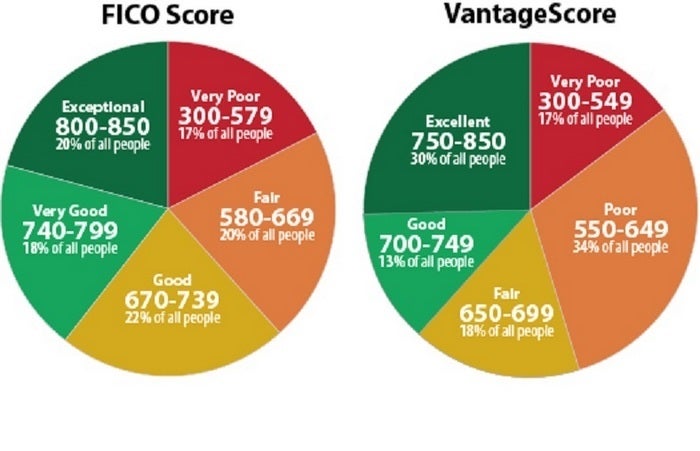

Three credit score reporting companies compile a credit score rating, however all three scores might not be the identical. The 2 commonest metrics for bank card approvals are Experian’s FICO rating and TransUnion’s VantageScore. You’ll be able to request your full credit score report without spending a dime as soon as per 12 months from every of the three bureaus (Experian, TransUnion and Equifax).

American Categorical, Uncover, USAA and Wells Fargo all permit you to examine your Experian FICO rating. Amex, Financial institution of America, Barclays, Capital One, Chase and U.S. Financial institution all permit you to examine your TransUnion VantageScore as effectively. You may also use just a few third-party websites, corresponding to Credit score Karma.

Every day E-newsletter

Reward your inbox with the TPG Every day publication

Be part of over 700,000 readers for breaking information, in-depth guides and unique offers from TPG’s consultants

Components that go into your credit score rating

Whereas every shopper credit score bureau calculates your rating a bit in a different way, just a few basic elements affect your rating, regardless of the company.

- Cost historical past — This makes up the biggest portion of your rating for FICO scores, however all three bureaus will have a look at your fee historical past. Collectors need to know that you’re a low-risk borrower, which suggests proving you’ll pay your payments on time.

- Debt-to-credit ratio — Primarily, this displays how a lot of your credit score line you utilize throughout accounts. An excellent rule of thumb is to try to maintain this ratio beneath 30% for a excessive credit score rating.

- Age of accounts — The longer your credit score historical past, the higher — which is why we usually encourage downgrading playing cards you now not use to no-annual-fee variations reasonably than canceling.

- New credit score — In case you’ve not too long ago opened a number of credit score accounts, it might negatively affect your rating as a result of it might probably point out potential monetary misery to collectors. This does not imply try to be cautious of opening new accounts altogether, however timing is one thing to think about.

- Credit score combine — Collectors need to see that you’ve got a mixture of credit score accounts, together with mortgages, automobile loans and extra. Do not take out loans you needn’t give your self a extra diverse combine, however do not forget that a well-managed automobile mortgage or mortgage might imply a better credit score rating.

Associated: 8 greatest elements that affect your credit score rating

What occurs if you happen to get rejected?

Getting rejected for a bank card is usually a bummer however it’s not the top of the world. Actually, many TPGers have been rejected for no less than one bank card of their lifetime. TPG contributor Ethan Steinberg has really been rejected for 12 totally different bank cards and nonetheless has a rating of about 780.

General, being rejected for a bank card should not do any long-term harm to your account. Whereas the “laborious inquiry” of the applying could ding your credit score rating just a few factors, your rating ought to bounce again after some time. You will not need to try to reapply for a similar card instantly, however you’ll be able to strive once more after three to 6 months.

In case you do get rejected, there’s a chance to get the choice reversed. You’ll be able to name the financial institution’s reconsideration line to ask for an enchantment (be sure to know what purpose the financial institution gave for the rejection earlier than you name). In case you clarify why you need/want the cardboard and the way you intend to make use of it, an agent could determine to approve you. Whereas there is no assure that you’re going to achieve success, it would not harm to (properly) ask.

Associated studying: How unhealthy is it to get denied for a bank card?

Backside line

Apply right here: Chase Freedom Flex

Apply right here: Chase Freedom Limitless