Whether or not you are a bank card rewards novice or a full-on knowledgeable, there are key tenets to comply with.

Because the saying goes, “Everybody makes errors,” and the factors and miles sport is not any exception. Whether or not you are brand-new to the passion or a seasoned professional, the potential for errors is all the time there.

On this information, I am sharing my 10 “commandments” for journey bank cards that will help you keep away from a number of the most typical errors made by cardholders.

Thou shalt pay thy steadiness in full

Conserving a steadiness is a cardinal sin in terms of bank cards.

Sadly, I do know a number of individuals who deal with credit score limits like free cash, spending at will with none definitive plan to pay the steadiness down. Other than being a surefire strategy to wreck your credit score rating (and damage your potential to open playing cards or acquire a mortgage or different mortgage sooner or later), this habits may also price you cash.

Most rewards bank cards carry high-interest charges — though a number of supply a 0% APR for an introductory interval — so working up a steadiness and never paying it off each month will negate the worth of any factors or miles you earn.

The right way to comply

Whether or not you’ve got one bank card or 20, all the time spend inside your means and keep organized. I exploit an Excel spreadsheet to undertaking out my checking account for a minimum of three months, so I do know that my outflows (funds, checks, and many others.) by no means exceed my inflows (earnings).

Thou shalt not miss a cost

Although not practically as dangerous as working a steadiness, lacking funds may be very pricey. For starters, most bank card issuers cost a late payment of $25-$35 in the event you submit a cost even a single day late. Though some bank cards could also be keen to waive the payment to your first missed cost, you’ll nonetheless need to keep away from it.

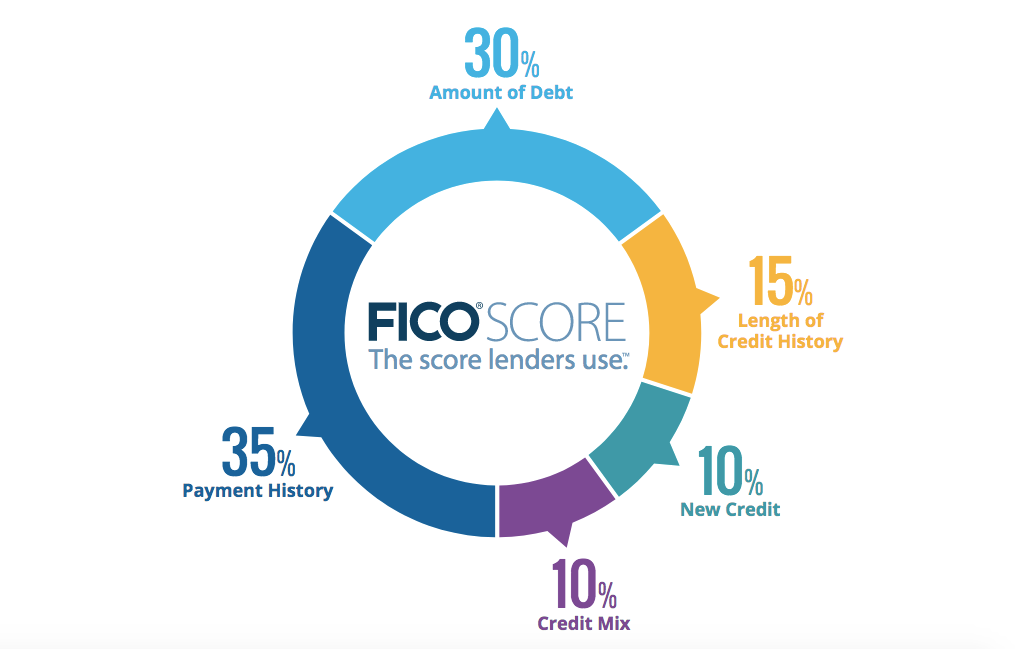

Funds made past your due date can even considerably have an effect on your credit score rating. Your cost historical past makes up over one-third of your total credit score rating, and whereas one missed cost is not deadly, a number of are a trigger for concern.

Day by day E-newsletter

Reward your inbox with the TPG Day by day publication

Be part of over 700,000 readers for breaking information, in-depth guides and unique offers from TPG’s specialists

Associated: What to do in case your bank card is delinquent — and how one can stop it from occurring

The right way to comply

Benefit from the automated cost options accessible on nearly each bank card.

After I open a brand new card, I set a calendar notification for 4 to 6 weeks later so I keep in mind so as to add my checking account and/or arrange automated funds. Do not forget that there could also be a one-to-two-month delay in activation, so you will have to manually make the primary one or two funds earlier than autopay kicks in.

Associated: The right way to arrange autopay to your bank cards

Thou shalt not cancel a card earlier than thou hast opened a brand new one

Many individuals are stunned by what number of bank cards I’ve, and I generally get requested, “Do not it’s good to cancel one card earlier than opening one other?” Completely not. Actually, canceling a card may very well damage your credit score rating.

There are two principal causes for this. For one, a big a part of your credit score rating (30%) consists of your credit score utilization ratio, or how a lot of your accessible credit score you truly use.

In the event you presently have balances of $5,000, and $50,000 of complete accessible credit score, your credit score utilization price is simply 10%. In the event you then cancel a card with a $30,000 restrict, your price all of the sudden jumps to 25% (as a result of your accessible credit score is now simply $20,000). That is not fairly within the hazard zone, however is excessive sufficient to present a card issuer some doubts.

Secondly, one other element of your credit score rating (10%) consists of your size of credit score historical past, and a part of this equation is the typical age of your accounts. For instance, in the event you’ve had a card with no annual payment for 5 or extra years, don’t cancel it. Make a number of purchases on it annually (so the financial institution does not shut it) and let it proceed so as to add to your historical past.

The right way to comply

Merely put, we advocate not canceling a card except doing so will not damage your credit score utilization price. If the cardboard has an annual payment that you simply need to keep away from, attempt to downgrade the cardboard to a no-annual-fee model as an alternative of canceling the cardboard.

Thou shalt not cancel a card and lose thy factors and miles

One other hazard of canceling a bank card is forfeiting the factors and miles you’ve got earned.

This is not a difficulty for a lot of bank cards related to a particular airline or resort chain, as what you earn routinely is credited to your loyalty account with that program. Nonetheless, different factors and miles merely sit with the cardboard issuer till you redeem them, together with American Categorical Membership Rewards factors and Chase Final Rewards factors.

Remember to redeem earlier than canceling playing cards with a lot of these rewards, as they may disappear as soon as your account is closed.

The right way to comply

Use the factors earlier than canceling the cardboard, both by transferring them to a associate or redeeming them straight for journey, assertion credit, and many others.

Thou shalt not permit thy rewards to run out

Whereas some loyalty packages (equivalent to JetBlue, Delta and United) do not put an expiration date on rewards, others will wipe out your account after a sure interval of inactivity.

That interval is mostly a minimum of 24 months, although it may be shorter.

The right way to comply

Thou shalt not miss out on a welcome bonus

Utilizing a rewards or journey bank card for day-to-day spending is an effective way to spice up your earnings all year long, however one of many largest drivers of bank card purposes is the sign-up bonus.

You possibly can miss out on an enormous inflow of factors by not spending sufficient within the specified time-frame (often three to 6 months). Some issues to remember in terms of these necessities:

- The clock often begins ticking as quickly as your utility is authorized: The timeframe to hit the bonus often does not begin while you obtain the cardboard; moderately, it begins instantly upon account approval. In the event you’re not sure of that date, name customer support to your card and ask.

- Annual charges, transferred balances and money advances don’t rely: For example, in the event you obtained in on the newest supply for The Platinum Card® from American Categorical, the $695 annual payment (see charges and charges) is not going to assist you to hit the minimal spending threshold.

The right way to comply

Figuring out the particular time-frame and what counts is half the battle, however you additionally want to trace spending. Spreadsheets, calendar reminders and cash administration instruments may be very useful for staying organized.

Associated: The very best time to use for these in style journey bank cards primarily based on supply historical past

Thou shalt reap the benefits of class bonuses

Many bank cards provide you with bonuses for purchases at sure retailers, together with eating places, supermarkets and gasoline stations. For example, I shudder when my pal pays for his or her dinner with a 1% cash-back card as an alternative of the Chase Sapphire Most popular Card or Chase Sapphire Reserve, each of which earn bonus Chase Final Rewards factors on eating purchases.

When you’ve got a card with bonus classes, be sure you use that card when making purchases in these classes.

Associated: The very best rewards bank cards for every bonus class

The right way to comply

Studying the cardboard settlement (or visiting the cardboard’s web site) to know the earnings and advantages offered by your present playing cards is a superb first step. You may as well take a look at our information to the perfect playing cards for every bonus class if you’d like a brand new card for a specific spending class.

Thou shalt not ignore playing cards with annual charges

In the event you’re new to this passion, chances are you’ll consider (as I as soon as did) that playing cards with an annual payment are horrible.

Nonetheless, many of those playing cards supply profitable sign-up bonuses, ongoing advantages and anniversary bonuses that greater than cowl the annual payment. As well as, lots of them waive the annual payment for the primary 12 months, providing you with a free one-year trial earlier than deciding whether or not to maintain the cardboard for the long run.

Associated: The whole information to bank card annual charges

The right way to comply

By visiting TPG, you’ve got already taken step one. Our knowledgeable evaluation will assist you to maximize your earnings and rewards on these playing cards, together with TPG’s month-to-month rating of the highest limited-time bank card provides. You may as well take a look at our greatest bank cards web page for a listing of those (and different) nice provides.

Thou shalt pursue retention bonuses

When you make the leap and open a card with an annual payment, there are nonetheless methods to keep away from the annual payment.

In the event you do not assume the worth you’ve got obtained from the cardboard justifies the annual payment, you possibly can all the time name your card issuer when the annual payment comes due and ask about waiving the annual payment.

Do not forget that the issuing financial institution desires you as a buyer, so it does not need you to shut your account. Many TPG readers (myself included) have obtained provides to maintain playing cards open, together with:

- A waived annual payment (no strings hooked up).

- Make X purchases in Y months and revel in a waived annual payment.

- Make X purchases in Y months and obtain Z bonus factors or miles.

- Z bonus factors or miles (no strings hooked up).

Associated: Professionals and cons of downgrading your bank cards proper now

I like to recommend doing this just for playing cards that you’d cancel with out getting a suggestion.

The right way to comply

Name the quantity on the again of your card when the annual payment comes up, and inform them that you simply’d prefer to cancel the cardboard because of the annual payment. Then, see what occurs.

Associated: My Amex Platinum retention bonus: 20,000 Membership Rewards factors

Thou shalt not pay international transaction charges

Many bank cards cost you a payment (usually 1%-3%) for each buy you make in a international forex or nation. This consists of purchases made overseas that the service provider converts to {dollars} for you (which it is best to by no means settle for, by the way in which).

However some bank cards waive these charges. A number of premium journey rewards bank cards haven’t got international transaction charges. Even some no-annual-fee playing cards (see charges and charges) just like the Capital One VentureOne Rewards Credit score Card waives international transaction charges (see charges and charges).

The right way to comply

This one is easy: Get a card that waives these charges. Listed below are the perfect bank cards with no international transaction charges.

Backside line

There are a lot of issues that you simply completely ought to (and shouldn’t) do regarding your journey rewards bank cards. Hopefully, this checklist of commandments has given you some meals for thought, whether or not you are searching for one of many finest cash-back bank cards or a premium journey rewards card.

Utilizing the factors, miles or money again to manifest a pleasant trip will ship a gratifying feeling. Nonetheless, it is important to benefit from each card you open and use it often.

For charges and charges of the Amex Platinum Card, please click on right here.