Paying your bank card balances in full each month is likely one of the 10 credit score commandments right here at TPG — not only for succeeding in journey rewards but in addition for sensible private finance.

Nevertheless, there could also be events when it’s good to make funds over time for bigger purchases and don’t need to pay excessive rates of interest for the power to take action. Enter “purchase now, pay later,” or BNPL, providers.

A comparability of purchase now, pay later providers

Most BNPL providers function equally. They do a mushy credit score examine to qualify you and decide your spending restrict, provide no curiosity charges and require you to make the primary fee on the time of buy. Usually, you’ll have three remaining funds, due each two weeks. You possibly can usually get instantaneous approval at checkout. And a few providers provide a digital card so as to add to your cellphone’s digital pockets to pay in-store.

With many BNPL providers accessible, it may be troublesome to tell apart between them and resolve which one to make use of. The notable variations between providers embrace buy limits, whether or not or not charges are charged for late funds and whether or not you’ll be able to pay in month-to-month installments (however you’ll typically should pay curiosity on this selection). We checked out Affirm, Afterpay, Klarna and PayPal, the highest 4 providers in line with a research by C+R Analysis. Since initially publishing this text, Apple Pay Later launched; we have added this as a fifth choice in our comparability.

Affirm

- The way it works: “Pay in 4” by making 4 funds (one each two weeks) or select a plan with month-to-month installments. You possibly can pay anyplace, even in-store, utilizing a one-time-use digital card.

- Compensation strategies: Checking account, debit card, bank card (however just for some purchases), examine funds by mail.

- Buy restrict: As much as $17,500.

- Credit score examine: Comfortable. Cost historical past, together with delinquent funds, could also be reported to Experian.

- Curiosity: No curiosity for the Pay in 4 plan; 0%-36% for the month-to-month funds plan.

- Late charges: None.

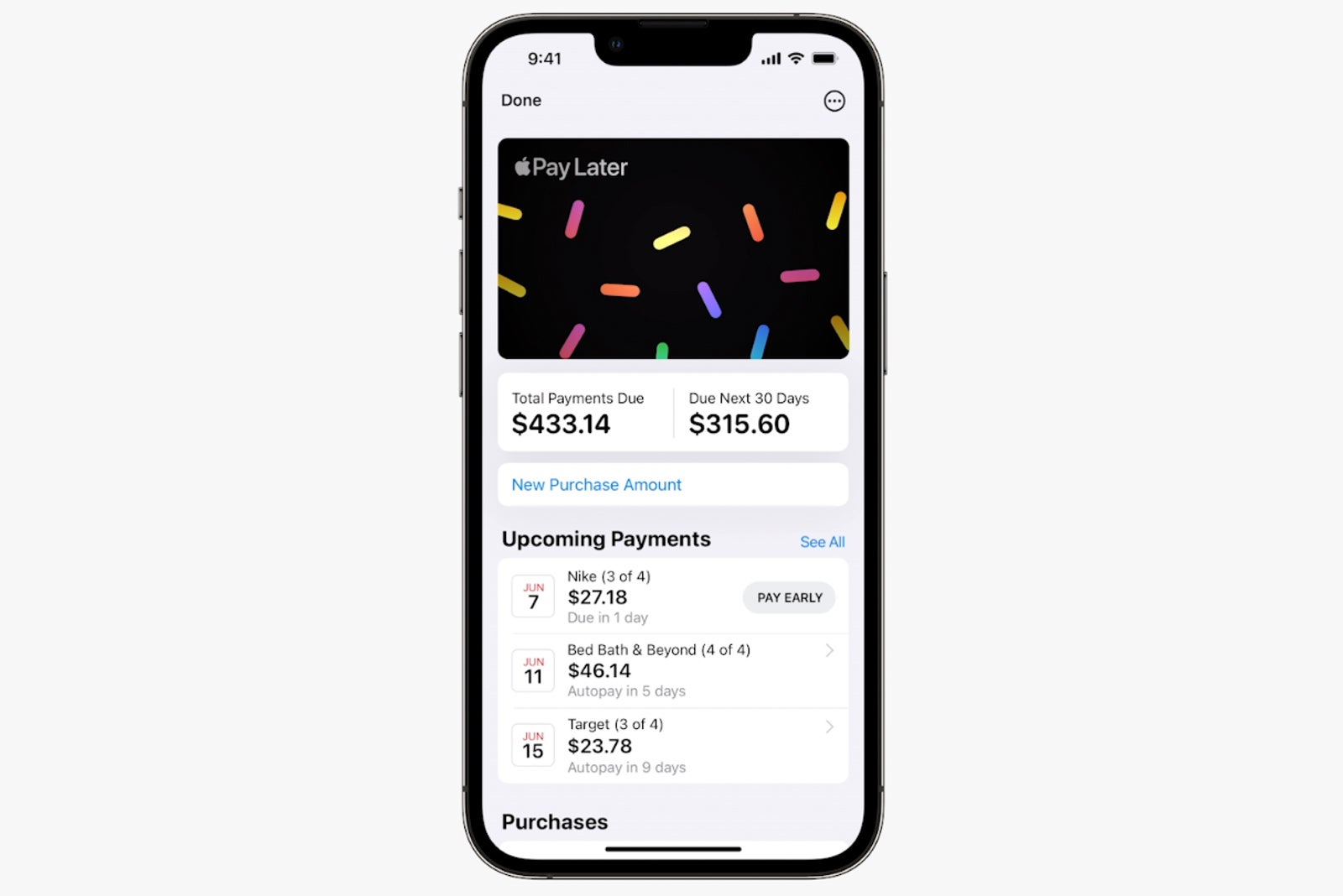

Apple Pay Later

- The way it works: Make the primary fee with buy, then three further funds over six weeks.

- Compensation strategies: Debit card.

- Buy restrict: As much as $1,000.

- Credit score examine: Comfortable; fee historical past could also be reported to credit score bureaus.

- Curiosity: None.

- Late charges: None.

Afterpay

- The way it works: Select fee plans of 4 interest-free funds (with the primary due at buy) or month-to-month installments of six or 12 months. In-store funds can be found with choose retailers, additionally.

- Compensation strategies: Checking account, debit card, bank card. Month-to-month installments can solely be paid by debit card.

- Buy restrict: Spending limits start at round $500 and enhance steadily over time.

- Credit score examine: Comfortable.

- Curiosity: None on the four-payment choice; varies on month-to-month installments.

- Late charges: Capped at 25% of the acquisition worth.

Klarna

- The way it works: “Pay in 4” with 4 interest-free funds, paid each two weeks. Extra choices embrace a no-interest “Pay in 30 days” plan and a month-to-month plan with versatile financing. Store on-line and pay with the Klarna app. To pay in-store, you’ll be able to create a single-use card and add it to your cellphone’s digital pockets.

- Compensation strategies: Checking account, debit card, bank card.

- Buy restrict: No predefined spending restrict. An automatic approval choice is made with each buy.

- Credit score examine: Comfortable for the Pay in 4 choice. Arduous for the month-to-month financing choice.

- Curiosity: None on Pay in 4 or Pay in 30 days choices; variable APR on month-to-month plans.

- Late charges: For the Pay in 4 choice, as much as $7 could also be charged for late funds after 10 days (to not exceed 25% of the installment fee quantity).

PayPal

- The way it works: The “Pay in 4” choice requires the primary fee to finish the acquisition, then three remaining funds (one each two weeks. Or go along with the newer “Pay Month-to-month” plan, the place the associated fee is damaged into month-to-month funds over a 6- to 24-month interval, with the primary fee due one month after buy.

- Compensation strategies: Checking account, debit card, bank card (your PayPal steadiness can’t be used for repayments, and bank cards cannot be used for Pay Month-to-month).

- Buy restrict: $30-$1,500 for Pay in 4; $199-$10,000 for Pay Month-to-month.

- Credit score examine: Comfortable for Pay in 4; Pay Month-to-month does a mushy examine for prequalification and a tough inquiry when a buyer accepts the mortgage and strikes ahead with financing choices.

- Curiosity: None for Pay in 4; 9.99%-29.99% for Pay Month-to-month.

- Late charges: None.

Do you have to use purchase now, pay later?

The simplicity of paying off a purchase order in 4 funds and never paying any curiosity expenses is interesting.

If you wish to maximize your factors and miles incomes, BNPL will not be ultimate. Although many providers let you hyperlink a bank card for compensation, you’ll lose out on any class bonuses you might have acquired from buying straight with the service provider.

As well as, utilizing one type of debt to pay one other type of debt isn’t clever, particularly for those who’re not in a position to repay the cost in your bank card when the invoice is due.

Moreover, C+R Analysis discovered that many individuals used BNPL providers to purchase objects they in any other case could not afford. This creates debt, provides further curiosity and may negatively have an effect on your credit score report.

Can I exploit my Capital One card for purchase now, pay later?

In the event you resolve to make use of a bank card for compensation, you gained’t be capable of use any Capital One bank cards because the financial institution blocks its playing cards for purchase now, pay later transactions. Nevertheless, Capital One debit playing cards and checking counts may be linked.

Join our every day e-newsletter

Associated: Are shoppers selecting ‘purchase now, pay later’ choices over bank card rewards?

Backside line

For bigger purchases that you just’d wish to repay over time however nonetheless need to earn rewards, contemplate bank cards with 0% introductory annual share charges and bank card providers equivalent to Chase’s My Chase Plan (no enrollment required) and Amex’s Pay It® Plan It® (no enrollment required). These provide installment plans with mounted month-to-month charges and no curiosity expenses.

Whichever BNPL service or bank card providing you resolve to make use of, accountable spending ought to stay the objective.

Associated: Different choices for vacation buy financing: My Chase Plan vs. Amex Pay It Plan It

Extra reporting by Ryan Smith.