So, certain: The Apple Card is not precisely a rewards behemoth.

In our full evaluation of the cardboard after its 2019 launch, we bemoaned its restricted perks, lack of a sign-up bonus and total failure to fulfill expectations after CEO Tim Cook dinner known as it “essentially the most vital change within the bank card expertise in 50 years.”

All that being mentioned, I needed to test it out alone and utilized on a whim. Months later, I nonetheless discover myself — a bank card novice however a TPGer nonetheless — utilizing the cardboard commonly.

Listed below are 4 the reason why the Apple Card may be best for you, too.

Easy incomes

It took me mere minutes to use for the Apple Card on my iPhone, and I have been glad ever since that the cardboard’s rewards construction is simply as easy.

The data for the Apple Card has been collected independently by The Factors Man. The cardboard particulars on this web page haven’t been reviewed or supplied by the cardboard issuer.

With the Apple Card, you earn 3% money again on all Apple purchases (together with tech merchandise, App Retailer purchases and different companies akin to Apple Music and Apple TV+), plus a lot of particular retailers. Proper now, these embrace:

- Ace {Hardware}.

- Duane Reade.

- Exxon.

- Mobil.

- Nike.

- Panera Bread.

- T-Cellular.

- Uber.

- Uber Eats.

- Walgreens.

You may additionally earn 2% money again on all purchases made with Apple Pay and 1% again on every little thing else.

As an Apple loyalist and Panera addict, I benefit from the 3% cash-back classes — however the 2% again with Apple Pay is the true winner for me. Almost each buy I make on-line may be made with Apple Pay, and whereas our evaluation famous that this card is “finest suited for individuals who stay in city areas,” I discover that increasingly in-store retailers are providing Apple Pay regardless of the place you end up.

Join our every day publication

The cardboard’s Apple Pay Household characteristic permits two companions to merge credit score strains and kind a single co-owned account. Each co‑homeowners can view and handle the account, see every member’s exercise and set limits on individuals’ spending.

On the spot rewards

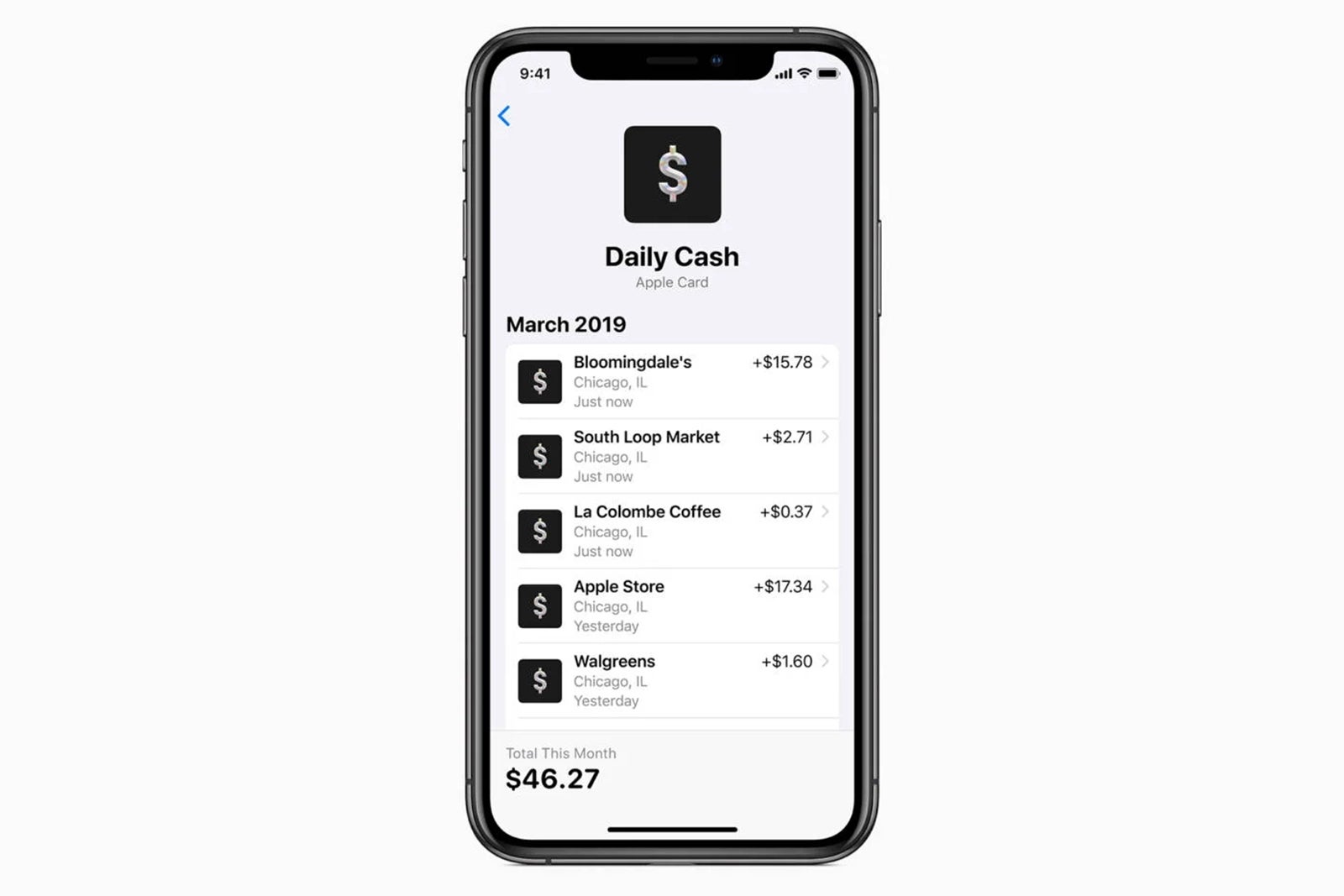

The Apple Card’s Every day Money system is constructed for the period of on the spot gratification.

Reasonably than ready till the top of a billing cycle to publish accrued month-to-month earnings, prospects who use the Apple Card will see cash-back totals every day, permitting you to make use of it immediately. I nonetheless get pleasure from saving up my money again, but it surely’s good to get common reminders about how a lot you earned the day prior to this.

Your Every day Money may also earn curiosity because it’s robotically deposited right into a high-yield financial savings account from Goldman Sachs, serving to your rewards develop over time.

The interface is constructed by Apple, that means it is easy and simple to make use of. By means of your Pockets app, you’ll be able to see earlier month-to-month statements, make a fee, test your out there stability and extra.

Every day Money and a clear, built-in interface are welcome adjustments from issuers who supply month-to-month money again and clunky third-party apps.

Zero charges

The Apple Card has completely no charges connected. Meaning no annual payment, over-the-limit charges, international transaction charges or late charges. As the cardboard web page guarantees, it actually has “No charges. Not even hidden ones.”

Apart from the plain proven fact that it is cheaper, I additionally benefit from the wall-to-wall simplicity of Apple’s strategy right here. Simply join in minutes, earn straightforward money again with Apple Pay and don’t fret about charges connected to touring overseas, going over your restrict and even making a late fee.

For those who’re a factors and miles professional, possibly none of this can be a massive deal to you. However as somebody nonetheless new to the area, I benefit from the peace of thoughts that comes with the Apple Card.

Superior privateness

And possibly a very powerful characteristic of all: The Apple Card goes above and past its rivals to guard your privateness and stop fraud. Most banks do not simply earn a living from charges and finance fees — additionally they revenue out of your private data.

Contemplate Financial institution of America’s U.S. shopper privateness coverage, which particulars the numerous methods it places details about a buyer’s creditworthiness and their transaction historical past within the palms of a variety of different corporations. Different banks, akin to Chase and Citi, have related insurance policies.

Apple says that Goldman Sachs, its accomplice for the cardboard, won’t share or promote your information to third-party corporations.

As for fraud prevention, the bodily card has no card quantity, safety code, expiration date or signature — simply your title and a chip. To entry these card numbers when making a purchase order on-line, cardholders want to drag up their card within the Pockets app. Moreover, the Apple Card incorporates a “one-time distinctive dynamic safety code” that adjustments after every buy you make, including one other layer of safety towards fraud.

Backside line

Like most rewards playing cards, the Apple Card is what you make of it. It would not supply essentially the most profitable rewards construction on the market, however should you’re an Apple loyalist or need a useful introduction to the bank card world, it could possibly be a match for you.

With a easy incomes construction and no charges connected, the cardboard is Apple to a T: streamlined, elegant and designed for essentially the most optimistic consumer expertise doable.