Editor’s be aware: This can be a recurring put up, usually up to date with new data.

At The Factors Man, we commit a big period of time to discussing how credit score scores work and how one can enhance your credit score rating. Scores within the mid-700s and above will usually be sufficient to get you authorized for many journey rewards playing cards. Nonetheless, having a decrease rating doesn’t essentially imply you could’t get these playing cards.

On this information, we’ll analyze information factors to uncover the unpublished (and maybe unofficial) credit score rating necessities for the ever-popular Chase Sapphire Most popular Card, which is at the moment providing an enhanced sign-up bonus of 80,000 bonus factors after you spend $4,000 on purchases within the first three months from account opening.

Simply be aware that though your credit score rating is an efficient indicator of your approval odds, it’s not an absolute science. Chase should still deny you even when you meet the “required” credit score rating — and should still approve you even when you’re beneath it.

Chase Sapphire Most popular overview

The Sapphire Most popular earns priceless Chase Final Rewards factors that may be transferred to this system’s resort and airline companions. It additionally comes with perks like an annual $50 resort credit score for reservations made by way of Chase Journey and a ten% factors bonus in your cardmember anniversary.

Take a look at the complete Chase Sapphire Most popular bank card overview for extra data.

Utility hyperlink: Chase Sapphire Most popular Card

Credit score rating wanted for the Chase Sapphire Most popular

Join our each day e-newsletter

Nonetheless, it’s definitely doable to be authorized for the Chase Sapphire Most popular as a newbie. Based on Credit score Karma, Chase Sapphire Most popular’s common required credit score rating is 736. The standard low rating is 646. So, whereas the common rating for approvals is “good” to “excellent,” excellent credit score historical past isn’t needed.

Many different elements go into qualification past your credit score rating, equivalent to your revenue and the common age of your credit score accounts. One other vital issue that’s typically forgotten is your relationship with the financial institution. If you happen to’ve been a longtime Chase buyer and have massive balances in your financial institution accounts with them, stories recommend that you’ll have higher approval odds (particularly when you apply in a department).

Lastly, even when you’re eyeing the Chase Sapphire Reserve, chances are you’ll wish to apply for the Chase Sapphire Most popular first. In any case, getting authorized for the Sapphire Most popular is usually simpler than the Sapphire Reserve. Additionally, making use of for the Chase Sapphire Most popular now will help you earn that sign-up bonus of 80,000 factors. Then, if you wish to make the most of the perks on the Sapphire Reserve at a later date, you possibly can request a product change.

Associated: Are you able to downgrade after which improve the identical card?

What number of card accounts can I’ve open?

The 5/24 rule is hard-coded into Chase’s system, so brokers usually can’t manually override it. As such, when you’re over 5/24, your solely choice for getting the Chase Sapphire Most popular is to attend till you’re underneath 5/24 once more.

Associated: The best way to calculate your 5/24 standing

The best way to examine your credit score rating

Not at all must you pay to examine your credit score rating. Many bank cards include a free FICO rating calculator. Additionally, there are numerous different methods to examine your credit score rating for completely free.

Many free websites will help you retain higher monitor of your rating and its elements. You may even use these companies to dispute any data in your rating that isn’t correct or seems to be fraudulent. You can additionally think about paying for a credit score monitoring service like myFICO.

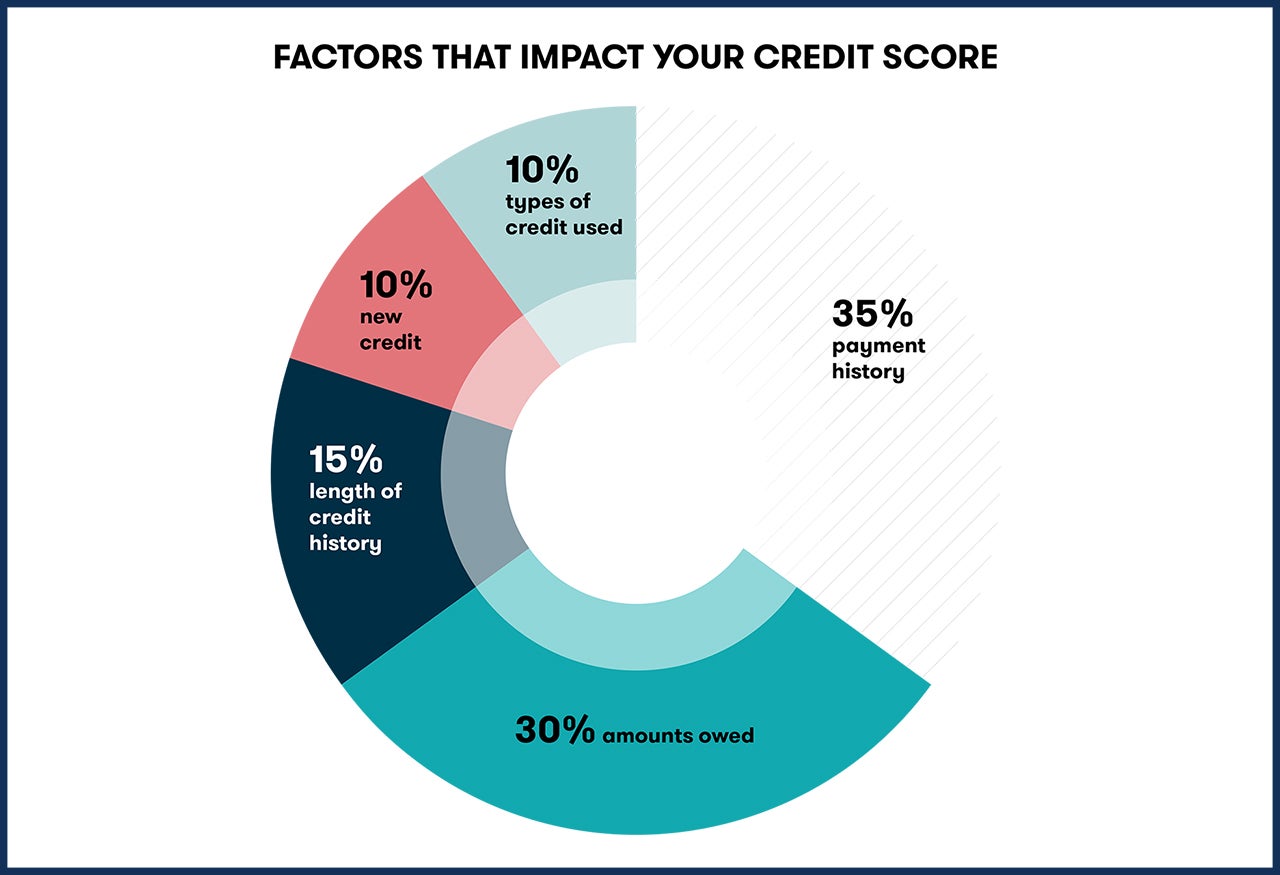

Elements that have an effect on your credit score rating

Earlier than you begin making use of for any bank cards, it’s important to know the elements that make up your credit score rating. In any case, the mere act of making use of for a brand new line of credit score will change your rating.

Whereas the precise method for calculating your credit score rating isn’t public, FICO is clear concerning the elements they assess and the weightings they use:

- Fee historical past: 35% of a FICO rating represents your cost historical past. So, when you get behind in making mortgage funds, this a part of your credit score rating will endure. Additionally, the extra prolonged and more moderen the delinquency, the extra vital the destructive impact.

- Quantities owed (credit score utilization): 30% of your FICO rating consists of the relative dimension of your present debt. Particularly, your debt-to-credit ratio is the overall of your money owed divided by the overall quantity of credit score accessible throughout all of your accounts. Many individuals declare that it’s finest to have a debt-to-credit ratio beneath 20%, but it surely’s not a magic quantity.

- Size of credit score historical past: 15% of your rating represents the common size of all accounts in your credit score historical past. The typical size of your accounts is usually a vital issue when you have a restricted credit score historical past. It will also be an element for individuals who open and shut accounts shortly.

- New credit score: Your most up-to-date accounts decide 10% of your credit score rating. So, this a part of your credit score rating will endure when you’ve not too long ago opened too many accounts. In any case, acquiring numerous new credit score is one signal of monetary misery.

- Credit score combine: 10% of your rating is said to what number of totally different credit score accounts you have got, equivalent to mortgages, automotive loans, credit score loans and retailer bank cards. Whereas having a mixture of mortgage sorts is healthier than having only one sort, nobody recommends taking out pointless loans solely to spice up your credit score rating.

With regard to the Chase Sapphire Most popular, one essential issue to think about is your common age of accounts. Whereas a lengthier credit score historical past will enhance your rating, many issuers concentrate on the one-year cutoff. That signifies that having a mean age of accounts of greater than a yr can go a good distance towards rising your odds of approval. Nonetheless, you might need bother getting authorized with 11 months of credit score historical past — even when your numerical credit score rating is great.

Lastly, when you have any delinquencies or bankruptcies in your credit score report, Chase would possibly hesitate to approve you for a brand new line of credit score. It’s vital to keep in mind that your credit score profile is greater than only a quantity. Certainly, your credit score profile is a group of data given to the issuer to research your creditworthiness.

In consequence, there’s no hard-and-fast rule with a particular credit score rating that may robotically get you authorized (or denied) for the Sapphire Most popular.

Associated: 7 issues to know about credit score earlier than making use of for a brand new card

What to do when you get rejected

When you’ve discovered why Chase rejected you, you possibly can name the reconsideration line. Inform the particular person on the telephone that you just not too long ago utilized for a Chase bank card, had been shocked to see Chase rejected your utility and wish to communicate to somebody about getting that call reconsidered. From there, it’s as much as you to construct a case and persuade the agent why Chase ought to approve you for the cardboard.

For instance, if Chase rejected you for having a brief credit score historical past, you possibly can level to your stellar file of on-time funds. Or, if Chase rejected you for missed funds, you would clarify that these had been a very long time in the past and your latest historical past has been excellent.

Associated: Your information to calling a bank card reconsideration line

Chase can also be recognized to restrict a buyer’s complete credit score line throughout all playing cards. You might have success overcoming a rejection by providing to shift unused credit score from an current card to the brand new one.

There’s no assure that your name will work, however about one-third of my rejections had been reversed on reconsideration. So, it’s price spending quarter-hour on the telephone if it’d make it easier to get the cardboard you need.

Backside line

- Have already got a Sapphire card (together with the Chase Sapphire Reserve and the no-annual-fee Sapphire card, which is now not accepting new candidates).

- Acquired a sign-up bonus from any Sapphire card within the final 48 months.

- Opened 5 or extra playing cards throughout all issuers within the final 24 months.

Though the common authorized credit score rating is comparatively excessive, you shouldn’t let that scare you away. In any case, Chase will think about many different elements. Your finest guess for retaining your rating on a profitable monitor is making on-time funds, retaining your closing balances low and being sensible concerning the accounts you open and shut. Establishing a banking relationship with Chase can even assist your case. Because the saying goes, although, your mileage could fluctuate.

Official utility hyperlink: Chase Sapphire Most popular Card

Extra reporting by Ryan Wilcox and Benét J. Wilson.