A standard query we get from rookies is in regards to the distinction between a “comfortable pull” and a “arduous pull” in your credit score report.

Each phrases are often used when discussing making use of for brand spanking new bank cards, however how does every have an effect on your credit score rating?

The foremost distinction between the 2 is {that a} arduous pull seems in your credit score report whereas a comfortable pull doesn’t. Let’s dig deeper.

What’s a tough pull?

While you apply for a line of credit score, whether or not it’s a new bank card, mortgage, auto mortgage or another kind of mortgage, the lender will pull your credit score report from at the least one of many three main credit score reporting companies — Equifax, Experian and TransUnion. That is known as a tough pull or a tough inquiry.

These checks are tied to an software and can seem in your credit score report. Meaning they might doubtlessly have an effect on your rating since new inquiries in your credit score report are a think about figuring out your credit score rating. What is taken into account an official software? Any time you ship in a request for a line of credit score and share your full identification particulars, resembling your identify, deal with and Social Safety Quantity.

A tough pull leads to the lender acquiring your official credit score report and credit score rating from whichever bureau it requested the knowledge. It is a rather more in-depth have a look at your credit score historical past than what may be collected and despatched over after a comfortable pull.

When are arduous pulls carried out?

As talked about above, arduous pulls are nearly at all times related to an software for credit score of some kind. Bank card issuers usually run arduous pulls once you apply for a brand new card (although there are some exceptions to this). Mortgage and personal scholar mortgage lenders may also run a tough pull in your credit score. Often, a possible landlord might ask to carry out a credit score examine. Relying on what service they use to run that examine, it might end in a tough pull.

Lenders will need a deeper have a look at your credit score report to make sure you’re a accountable borrower and more likely to repay the quantity of credit score you request.

Associated: Final information to bank card software restrictions

Every day Publication

Rewarding studying in lower than 5 minutes

Be part of over 700,000 readers for breaking information, in-depth guides and unique offers from TPG’s specialists

What’s a comfortable pull?

A comfortable inquiry doesn’t seem in your credit score report and doesn’t have an effect on your rating in any respect. Comfortable pulls usually happen once you examine your credit score rating otherwise you give somebody, like a possible employer, permission to evaluate your credit score report.

Typically talking, a comfortable pull will not end in somebody receiving your full credit score profile and rating. As an alternative, they may get an estimated rating based mostly on the knowledge requested or might get restricted info on only one space of your report.

These credit score checks usually are not tied on to a credit score software of any type, which is why they are not recorded in your report and don’t have an effect on your credit score rating.

When are comfortable pulls carried out?

Any time you or somebody you give permission to examine your credit score rating and it is not tied to an official software, it would probably end in a comfortable pull. Typically, a comfortable pull will not end in a full, in-depth report being shared with the recipient.

For instance, checking your credit score by means of a service resembling Credit score Karma leads to a comfortable pull. Moreover, when insurance coverage corporations request a credit score examine to present you a quote, that may often additionally end in a comfortable pull.

Whereas opening new credit score accounts leads to a tough pull, pre-qualified provides usually solely requires a comfortable pull. Card issuers or different lenders might supply to carry out one to present you perception into your approval odds earlier than you submit an official software.

If you’re working to enhance your credit score rating and are cautious of any nonessential arduous inquiries being listed in your account, pre-qualification instruments that do not have an effect on your credit score rating in any respect may be helpful. Moreover, you need to use pre-qualification instruments resembling CardMatch to seek out the most effective welcome provides obtainable throughout sure bank cards with focused provides.

How do arduous pulls have an effect on your credit score rating?

Arduous pulls in your credit score report sign that you simply need to open a line of credit score. The extra inquiries you will have in a brief time frame, the extra collectors would possibly assume you’re in monetary misery and, subsequently, at the next danger for delinquencies. Each the FICO and VantageScore credit score scoring fashions think about latest credit score habits, together with new inquiries. This will have an effect on your rating in two methods.

While you apply for a brand new account, it’s possible you’ll discover a slight dip in your rating due to the arduous pull. That is nearly at all times non permanent and may solely have an effect on your rating by a number of factors at most.

Nevertheless, in case you have opened many new credit score accounts lately, that would have an effect on your rating in the long run. Arduous inquiries can keep in your credit score report for as much as two years, which signifies that’s how lengthy they will doubtlessly have an effect on your rating.

Arduous pulls additionally issue into your Chase 5/24 eligibility.

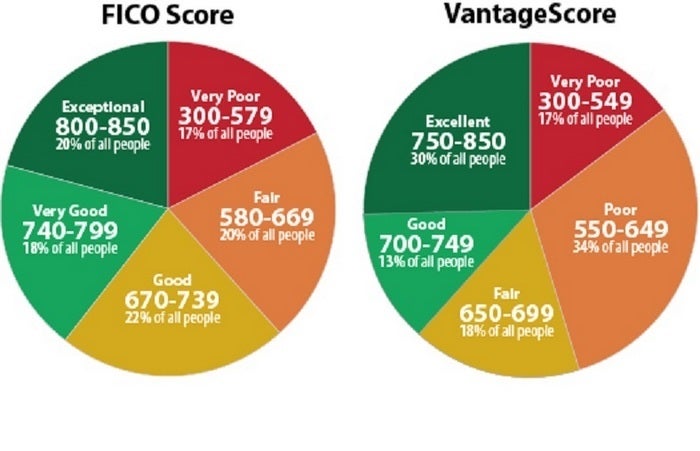

Associated: What is an effective credit score rating?

What number of arduous pulls are too many?

In response to Credit score Karma’s credit score rating service, holding latest inquiries under two is perfect. You begin to drift into the “crimson zone” after you have 5 or extra in your account.

Take this with a grain of salt, although. FICO solely makes use of new inquiries to make up 10% of your rating, and TransUnion lists credit score habits and new accounts as a “much less influential” issue. Many TPG staffers have seven or eight inquiries on their studies and nonetheless have wonderful credit score scores.

Whilst you’ll need to keep away from pointless inquiries in your account, do not let the potential of having one other arduous pull in your report cease you from making use of for a brand new bank card in case your rating is in any other case wholesome.

Associated: Ought to I apply for a bank card now?

Backside line

Keep in mind that whereas arduous inquiries can have an effect on your credit score rating, they solely make up a small proportion of your total rating. So long as you will have a confirmed historical past of paying payments on time and never overutilizing your traces of credit score, a brand new inquiry should not negatively have an effect on your rating in the long run.

Further reporting by Danyal Ahmed, Stella Shon and Benét J. Wilson.